What Is the Cash Value of Life Insurance After 20 Years?

Life insurance policies, particularly permanent life insurance, offer more than just a death benefit. One of their most appealing features is the cash value component, which can accumulate over time. For those who hold a life insurance policy for 20 years, understanding how the cash value works and its potential benefits is essential. Here’s a breakdown of what you need to know about the cash value of life insurance after two decades.

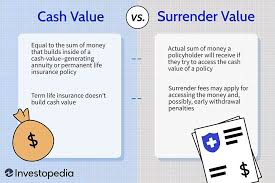

What Is Cash Value in Life Insurance?

Cash value is a feature of permanent life insurance policies, such as whole life, universal life, and variable life insurance. Unlike term life insurance, which only provides a death benefit, permanent life insurance accumulates a savings component. This savings grows over time, tax-deferred, and can be accessed by the policyholder while they are alive.

The cash value is built using a portion of the premiums you pay. After the cost of the insurance and any associated fees are covered, the remainder is deposited into the cash value account, where it grows based on the policy type:

- Whole life insurance: The cash value grows at a guaranteed rate set by the insurer.

- Universal life insurance: Growth depends on interest rates, which can vary.

- Variable life insurance: The cash value depends on the performance of investment options you select.

Factors Affecting Cash Value After 20 Years

Several factors determine how much cash value your policy will have after 20 years:

- Policy Type: Different types of permanent life insurance accumulate cash value at different rates. Whole life policies generally provide steady growth, while variable life policies may offer higher returns but come with more risk.

- Premium Payments: The amount you pay in premiums and how consistently you pay them affects the growth of your cash value. Higher premiums typically lead to greater cash value accumulation.

- Fees and Charges: Insurers deduct fees and the cost of insurance from your premiums before adding to the cash value. Policies with lower fees will accumulate cash value more quickly.

- Loan or Withdrawal History: If you’ve taken loans or withdrawals against the cash value, this reduces the amount that accumulates over time.

- Dividends: Some whole life policies pay dividends, which can be used to increase cash value, reduce premiums, or even purchase additional coverage.

Estimating Cash Value After 20 Years

While it’s difficult to provide a universal figure, here’s a general idea based on policy types:

- Whole Life Insurance: After 20 years, the cash value might be close to or slightly higher than the total premiums paid, depending on the policy’s guaranteed growth rate and any dividends received.

- Universal Life Insurance: The cash value will vary based on interest rates. A policyholder might see modest to significant growth depending on market conditions.

- Variable Life Insurance: With investment-based growth, the cash value could be much higher or lower than premiums paid, depending on the performance of chosen investments.

To get a precise estimate, review your policy’s illustration or consult your insurance agent.

How to Use Cash Value After 20 Years

After 20 years, your policy’s cash value can serve several purposes:

- Supplemental Income: You can withdraw from or borrow against your cash value to fund retirement, pay for a child’s education, or cover emergencies. Keep in mind that loans reduce the death benefit if not repaid.

- Premium Payments: You can use the accumulated cash value to cover future premium payments, ensuring the policy remains in force without additional out-of-pocket expenses.

- Policy Surrender: If you no longer need the coverage, surrendering the policy allows you to access the cash value, minus any surrender charges. However, this terminates the policy.

Key Considerations

- Tax Implications: Withdrawals and loans are generally tax-free, but surrendering the policy or withdrawing more than the total premiums paid could result in taxable income.

- Impact on Death Benefit: Using the cash value may reduce the death benefit your beneficiaries receive.

- Surrender Charges: These fees may apply if you terminate the policy within a certain timeframe, though they often diminish over the years.

Conclusion

The cash value of a life insurance policy after 20 years can be a significant financial asset, offering flexibility and security. To maximize its potential, it’s important to understand your policy’s terms, monitor its performance, and use the cash value wisely. If you’re unsure about the specifics of your policy, consulting with a financial advisor or insurance professional can provide clarity and help you make informed decisions.